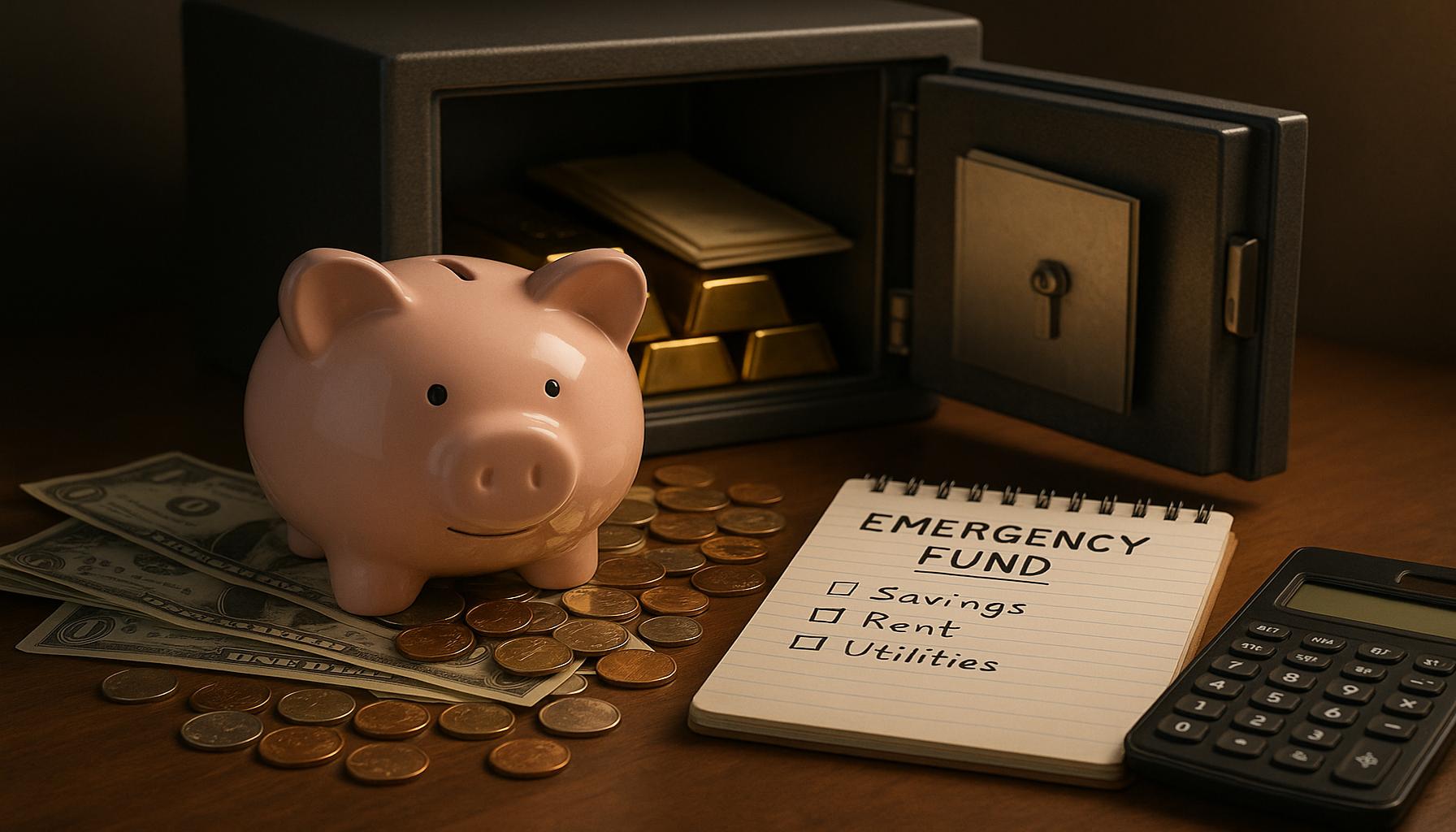

The Importance of Creating an Emergency Fund for Financial Security

Why an Emergency Fund is Essential

Unexpected expenses can arise at any moment, making it essential to have a financial plan that incorporates a safety net. One of the most effective strategies for achieving this is by building an emergency fund. This fund serves as a financial cushion, enabling individuals and families to manage unforeseen costs without derailing their financial stability.

Scenarios Highlighting the Need for an Emergency Fund

There are several instances where having an emergency fund can make a significant difference:

- Medical emergencies: Health issues can occur without warning, often resulting in high medical bills. For instance, a sudden hospitalization may require immediate out-of-pocket expenses that can quickly accumulate.

- Job loss: An unexpected layoff can create an income gap, leaving you struggling to cover monthly expenses like rent or utilities. Without an emergency fund, you may be forced to rely on credit cards, which can lead to spiraling debt.

- Urgent home or car repairs: Whether it’s a burst pipe or a malfunctioning car, certain repairs cannot be delayed. An emergency fund allows you to address these issues promptly and avoid further complications.

The Benefits of an Emergency Fund

Establishing an emergency fund not only allows for reactive problem-solving; it also fosters strategic decision-making during financial crises. When you have access to funds when necessary, you can make choices that align with your long-term goals instead of succumbing to panic. This financial resilience helps maintain your independence, as it reduces your reliance on expensive borrowing options.

Long-Term Financial Goals and Stability

A well-stocked emergency fund contributes significantly to your overall financial health:

- Peace of mind: Knowing you have a financial safety net reduces anxiety associated with money management, allowing you to plan for the future with confidence.

- Focus on investments: With an emergency fund in place, you can prioritize savings and investments, giving you the freedom to explore opportunities such as retirement accounts or stock investments without fear of immediate cash flow issues.

- Healthier financial habits: The process of building an emergency fund encourages disciplined saving, which reinforces positive spending behaviors that are beneficial for long-term wealth accumulation.

By prioritizing the establishment of an emergency fund today, you are setting the foundation for a more secure future. This proactive approach enables you to navigate the inevitable uncertainties of life while remaining focused on your broader financial objectives, ultimately contributing to long-lasting financial well-being.

DISCOVER MORE: Click here for insights on mortgage loan rates

Understanding the Mechanics of Building an Emergency Fund

Establishing an emergency fund is not just about setting money aside; it’s a strategic aspect of financial planning that lays the groundwork for stability and future growth. To create a robust emergency fund, one must first assess their current financial situation and then set clear, actionable goals. This involves understanding your monthly expenses and determining a target amount that can effectively cover unforeseen events, such as sudden medical bills, unexpected car repairs, or abrupt job loss.

Determining the Right Fund Size

The size of your emergency fund is crucial and will vary based on individual circumstances. A general rule of thumb is to aim for three to six months’ worth of living expenses. However, those with dependents, homeowners, or variable incomes might consider saving up to a year’s worth of expenses to ensure greater security. Assessing your situation requires careful evaluation of several critical factors:

- Monthly expenses: Calculate your essential expenses—housing, utilities, transportation, food, and healthcare. This forms the baseline for your fund. For instance, if your calculated monthly expenses total $3,000, planning for at least $9,000 to $18,000 would provide a healthy cushion.

- Income stability: If you work in a fluctuating field or are self-employed, a larger cushion may be necessary to weather income instability. A freelance graphic designer might face inconsistent income, making it beneficial to aim toward the higher end of the spectrum with six to twelve months of expenses saved.

- Dependents: Families with children are generally advised to have a more substantial emergency fund, as unexpected costs can multiply when you have dependents to consider. Childcare issues, medical emergencies, or educational expenses can all arise, adding to the need for a robust safety net.

Strategies for Building Your Fund

Once you’ve determined the ideal size of your emergency fund, the next step is to employ effective strategies for building it. Consistency and disciplined saving are vital components of this process. Here are several approaches to consider:

- Automate savings: Set up automatic transfers from your checking account to a separate savings account designed exclusively for your emergency fund. This “pay yourself first” approach ensures that you prioritize saving. Even a small monthly contribution can accumulate significantly over time.

- Cut non-essential expenses: Review your spending habits and identify areas where you can reasonably cut back—be it dining out less frequently, canceling unused subscriptions, or adjusting your entertainment budget. Redirect these savings into your emergency fund. For example, saving $50 a month by reducing dining out can lead to an additional $600 saved in a year.

- Utilize windfalls: Use bonuses, tax refunds, or other unexpected income to give your emergency fund a significant boost. This can expedite your path to financial security. For instance, if you receive a tax refund of $1,500, consider depositing that amount directly into your emergency fund instead of spending it.

Implementing these strategies requires commitment, but the long-term benefits significantly outweigh the short-term sacrifices. By consistently building your emergency fund, you establish a financial buffer that prepares you to face life’s uncertainties with greater confidence. This proactive approach not only safeguards you during tough times but also supports your long-term financial goals, allowing for more freedom and creativity in investments and savings strategies. Ultimately, having an emergency fund is not just about preparedness; it is fundamentally linked to your ability to seize new opportunities and pursue a financially secure future.

DISCOVER: Click here for quick money options

The Psychological Benefits of an Emergency Fund

Establishing an emergency fund offers more than just financial security; it can significantly enhance your overall psychological well-being. The peace of mind that comes with having a financial safety net is a powerful motivator, allowing individuals to pursue their goals and aspirations without the constant fear of unexpected setbacks. Understanding this emotional aspect is essential to appreciating the full value of an emergency fund.

Reduced Stress and Anxiety

Financial uncertainty is a leading cause of stress for many individuals and families. The looming threat of unexpected expenses can create anxiety that affects daily life and decision-making. Having an emergency fund can mitigate this stress substantially. When you know that you have saved a specific amount to fall back on, you are less likely to feel overwhelmed during challenging times. For example, if your car unexpectedly breaks down and you have a dedicated fund for such emergencies, you can handle the situation without resorting to credit cards or high-interest loans, which can exacerbate financial strain.

Improved Financial Decision-Making

With the safety net of an emergency fund, individuals can make financial decisions with greater clarity and confidence. This security allows you to avoid hasty, reactive choices that often arise from financial panic. Instead of feeling compelled to accept the first job offer that comes your way or being forced to dip into retirement savings during a crisis, you are empowered to seek out the right opportunities that align with your career goals. As a result, the long-term impacts of smart decision-making will pave the way for greater stability and potential growth.

Cultivating Long-Term Financial Habits

Building an emergency fund cultivates beneficial financial habits that extend beyond just saving for emergencies. The discipline required to consistently contribute to your fund can foster an overall mindset of financial prudence. This approach not only applies to building your emergency fund but also encourages proactive saving for retirement, investments, and other financial goals. As you witness your emergency fund grow, you become more attuned to your financial health and more motivated to prioritize other aspects of financial security, such as contributing to retirement accounts like a 401(k) or an IRA.

Empowerment and Financial Independence

Achieving financial independence is a goal for many people, and an emergency fund is a cornerstone of that journey. By systematically saving and accumulating an emergency fund, you gain the independence to make choices that enhance your quality of life. This kind of financial empowerment allows individuals to take calculated risks, whether in their careers, education, or investments—all while knowing that they have a safety net to catch them if needed. Having an emergency fund can transform your perspective from survival mode to a state of growth and opportunity.

Encouraging Resilience Against Financial Setbacks

Life is inherently unpredictable, and financial setbacks can occur at any time. However, having an emergency fund creates resilience, enabling you to bounce back more readily from life’s challenges. In fact, studies indicate that individuals with emergency savings experience less financial volatility than those without. A well-funded emergency fund primes you for endurance, giving you the confidence to tackle obstacles head-on rather than succumbing to financial distress.

Through these psychological benefits, it becomes clear that an emergency fund is not merely a financial tool; it is a catalyst for fostering better mental health and a more empowered approach to personal finance. The ability to face adversity not only stabilizes your current situation but also aids in shaping a confident mindset for future financial pursuits.

DISCOVER MORE: Click here to save big on your next shopping trip

Conclusion

In today’s unpredictable financial landscape, the significance of establishing an emergency fund cannot be overstated. It serves as a critical pillar of financial security, offering safeguards against life’s unforeseen challenges, such as medical emergencies, job loss, or urgent repairs. Beyond just monetary advantages, an emergency fund enhances your overall mental well-being by reducing stress and anxiety. With a dedicated financial buffer, you can approach life’s uncertainties with a clear mind, make informed decisions, and refrain from impulsive actions that may jeopardize your financial future.

Furthermore, cultivating an emergency fund encourages vital financial habits such as consistent saving and disciplined spending. This practice not only positions you for immediate financial resilience but also lays the groundwork for achieving long-term goals like retirement savings and investments. By viewing your emergency fund as both a safety net and a stepping stone, you harness the empowerment of financial independence, paving the way for opportunities that align with your aspirations.

As you navigate your financial journey, prioritize establishing and growing your emergency fund. Start small, but aim for at least three to six months’ worth of expenses. This comprehensive preparation will not only enrich your present circumstances but also create a trajectory towards lasting financial stability and security for years to come. Remember, today’s financial decisions have a profound impact on your future, so invest in your peace of mind and resilience by making an emergency fund a central aspect of your financial planning.

Linda Carter

Linda Carter is a writer and expert known for producing clear, engaging, and easy-to-understand content. With solid experience guiding people in achieving their goals, she shares valuable insights and practical guidance. Her mission is to support readers in making informed choices and achieving significant progress.